Where to Park Idle Startup Cash: Choosing Your Anchorage Between Safe Harbor and Open Water

Where to park idle startup cash comes down to one choice: how far from safe harbor you anchor for a little more yield, knowing open water pays better and sinks faster.

Where to park idle startup cash is really a question about distance: how far out from safe harbor are you willing to anchor for a little more yield? Stay tied up at the dock and you earn next to no return, but next to nothing can reach you either. Sail out past the harbor entrance and the water pays better, and it can also put the boat on the rocks. At each spot where you drop anchor, you trade one for the other. The answer is not a single account or instrument. It is a course you pick on purpose.

Most founders treat idle cash like a boat they tied off and forgot about. The round closes, the money lands in checking, and it sits there losing value to inflation while the captain looks the other way. That is not safety. It is drift, with the anchor never set.

Read the water before you drop anchor

A good captain checks the depth and the bottom before letting go of the rode, because sand holds and bare rock does not. You want to know what is under you before you count on it to hold the boat overnight.

Cash works the same way. Before you decide where to park it, you sound your own position: how much must reach payroll this week, how much covers the next few months if a customer pays late, and how much is truly free. Keynes put it in simple terms a long time back. A business holds cash for three reasons: to pay the bills as they fall due, to keep a reserve against an unexpected gap, and to hold value until it decides where that value should work. Those three jobs sit at three different distances from shore. Mix them in one checking account and you cannot tell which money does what, which is the same as anchoring in the dark.

For the cash a startup cannot afford to lose, the first rule is return of capital, then return on capital. Get the order wrong and a good month of yield will not buy back a payroll you could not run.

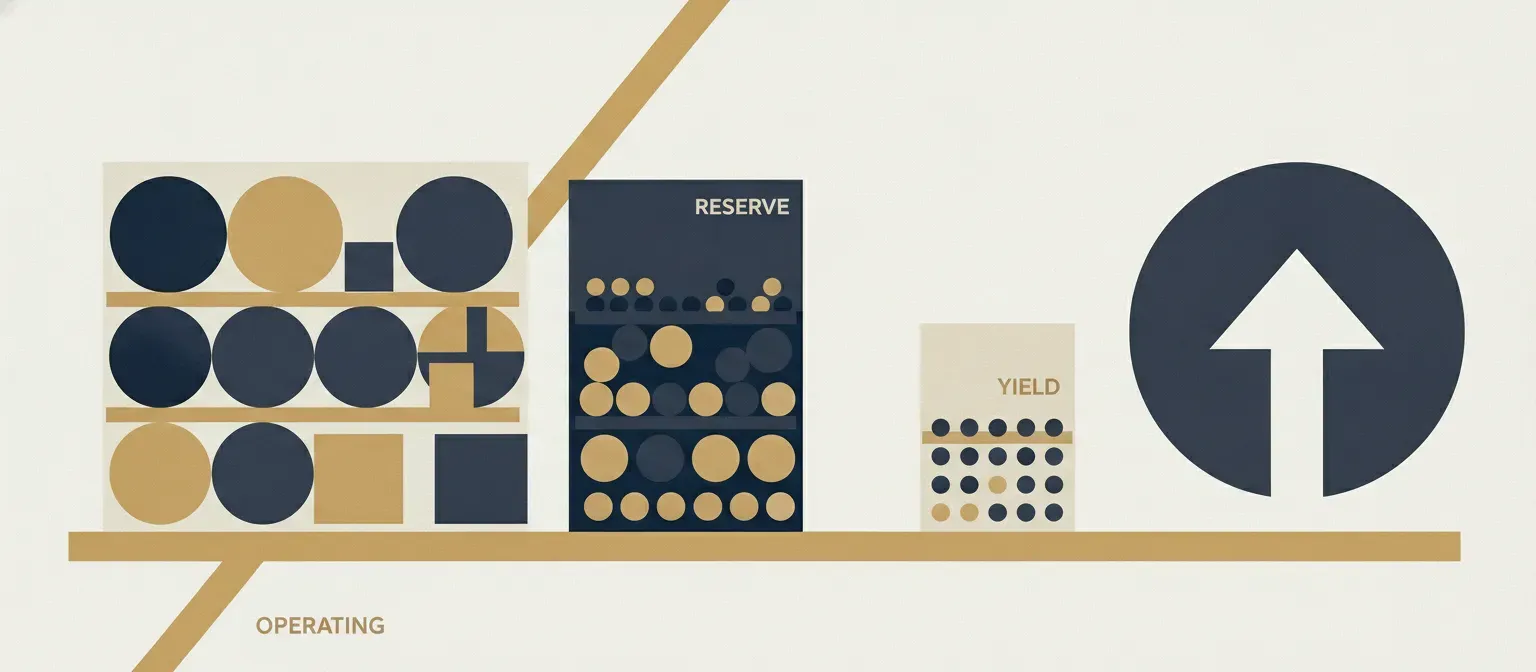

The dock: cash that stays in safe harbor

Some of your money never leaves the harbor, and it should not. This is the operating cash you spend in the normal course of business: payroll, suppliers, the software bills that fall due every week. It needs to be there the instant you reach for it, with no maturity to wait on and no risk to the value of the asset.

Where it sits: a business checking account at a bank with deposit insurance. That is the whole answer. Do not get clever at the dock.

How much: roughly one to two months of operating expenses. Build that number from a real cash flow forecast, not a gut feel. The direct method works well over a 30-day horizon because you schedule the actual receipts and disbursements instead of guessing at them. Know what comes in and what goes out, and the buffer stops being a number you made up.

Just outside the harbor mouth: the near-term reserve

The next mooring is a short sail from the dock. Still protected, still within sight of land, but earning a little while it waits. This is your precautionary money. It covers the months when a customer pays late or a round slips, so you never have to raise cash from a poorer spot at a poorer time.

Where it sits: short-maturity cash equivalents. Money market funds, treasury bills, certificates of deposit. By definition a cash equivalent carries an insignificant risk of changes in value and converts to a known cash amount fast, usually with a maturity of 90 days or less. Low risk, low return, and that is the point of the reserve, not a flaw in it.

How much: three to six months of operating expenses on top of the dock. Tie it to your forecast and your appetite for surprises. A company with poor visibility into its own receipts needs a larger reserve than one with collections it can chart in advance.

The far anchorage: longer idle cash that works

Now we are past the harbor mouth, in deep water, with the boat well anchored and the chain set long. Out here, cash either has a job or it loses value to inflation because you never gave it one.

There is no such thing as truly idle cash.

If you raised a large round, the money beyond your buffer and reserve sits out here, working, not resting at the dock while prices rise. But see where we still are. Anchored. Protected. We sailed for more yield, not into open water.

Where it sits: still inside the conservative box, just set for return now that safety and access are handled. A long line of treasury bills set to mature in turn, money market funds, sweep accounts that move free funds into an interest-bearing vehicle overnight and back the next morning. A sweep is worth its place here, because the money has time to rest.

How much: whatever is left once the dock and the reserve are full. For a well-funded startup that can be most of the balance. The rule is direction, not a fixed split: safety first, access second, yield third, never out of that order.

Why open water is a danger, not an upgrade

Out past every mooring is open water, where the real returns sit and where boats are lost. Equities, long-dated paper, anything you cannot turn back into cash on a bad day. The yield is real. So is the chance that the value drops the same week you need the money, and you sell at the bottom to make rent.

Liquidity risk is just this, in finance terms: the chance you cannot trade an asset fast enough when you need it. A startup that sails the months of cash it runs on into open water for an extra point is one bad tide from the rocks. Picture a seed-stage team that puts nine months of operating cash in a fund holding the money for 60 days. A vendor invoice and a slow customer hit in the same week, and now they are borrowing against a credit line at a poorer rate than the yield they reached for. The sea does not care how clever the spreadsheet looked in fair weather.

Actually, let me correct one thing. The danger is not the open water itself. It is sailing operating and reserve cash into it. The far anchorage can hold a long line of yield-bearing instruments and still be safe, because the boat anchored there has time and protection. Distance without those two is how you lose the hull.

How much, and where the lines fall

Each mooring shows you where. Your forecast shows you how much. Run a week-by-week projection of net cash flows. Any period that falls into a large negative shows you how deep the dock and the reserve must be. Everything above that line can sail to the far anchorage and earn.

Two rules keep the whole thing honest. First, spread your providers and respect insured limits, so no single bank failure can reach across every mooring at once. The real problem is concentration and inattention, not banks as a category. Second, keep all your positions on one chart. The moment you cannot see every mooring at a glance, the system stops protecting you, and that blind spot is exactly what a consolidated cash-position monitor closes.

Frequently asked questions

Where should a startup park idle cash to earn interest?

Park it in conservative cash equivalents once the operating buffer and reserve are full: money market funds, short-maturity treasury bills, certificates of deposit, or a sweep account that earns overnight. These carry low risk and a known value, so the money works without putting the cash you run on at risk. Stay anchored in protected water, not out in equities.

How much startup cash should stay in checking?

Keep about one to two months of operating expenses in business checking, set from a real cash flow forecast rather than a round number. That is your dock: payroll, suppliers, and bills as they fall due. All cash beyond it should sail out to the reserve or the far anchorage to earn instead of resting at zero.

Is it safe to park all idle startup cash in one bank account?

No. One account buries which dollars are committed and ties your whole exposure to a single bank failure. Split the cash by job and distance, spread your providers, and respect deposit insurance limits so concentration never becomes the hazard that grounds the boat.

Should a startup reach for higher yield with idle cash?

Only with the far anchorage, and only after safety and access are set. Reaching for yield with operating or reserve cash is one of the worst moves a founder can make on the water. Return of capital comes before return on capital, full stop.

The stand

Founders should anchor on purpose, not tie off and look away. Open water pays the most and takes the most, and the cash that keeps a company running has no business out there. Pick three moorings, give each one a job and a distance, size each from a real forecast, and you keep your cash safe, reachable, and earning in the right order. That only holds if you can see every position on one chart. CX Cash gives every dollar a job and holds all three positions in a single view. You should know where the money is going. Start with our consolidated cash-position tracker, sort your cash by job and distance this week, and tell another founder still anchored in the dark to do the same.

More in Cash & Treasury Management

Cash Position 101: The Schrödinger's Cat Sitting In Your Bank Accounts

Until you look at every account, your cash position is both alive and dead at once. Here is how the act of looking collapses it into one real number you can use.

Treasury management is your company's bloodstream, not a Series C luxury

Treasury management is the circulatory system of a business: the system that decides which parts get cash and when. It keeps your company solvent at any size, even at zero revenue.